From Reactive to Ready: How New Financial Risk Management Tools like Pillar Empower Small Businesses and Legal Practices

Volatile cash cycles, rising payment fraud, and tightening regulatory expectations have made financial risk a daily operating concern for small businesses and legal practices. Yet most firms still manage risk with spreadsheets, manual reconciliations, and gut feel—leaving blind spots that surface only when cash is tight or an audit looms. A new generation of financial risk management tools—exemplified by platforms like Pillar—brings enterprise-grade visibility, automation, and governance to smaller organizations. The payoff: steadier cash flow, cleaner audits, and fewer expensive surprises. This article explains what’s changed, how these tools work, and a practical blueprint to deploy “RiskOps” in 90 days without derailing the work that pays the bills.

- Why Financial Risk Management Is Different Now

- What Modern Tools Like Pillar Actually Do

- Use Cases: Fast Wins for Small Businesses and Legal Practices

- Your RiskOps Blueprint: A Lightweight, Durable Stack

- Implementation Roadmap and ROI Modeling

- Governance, Compliance, and Vendor Selection Pitfalls

Why Financial Risk Management Is Different Now

Risk used to arrive on a quarterly schedule: you closed the books, looked backward, and hoped nothing broke. Today, risk is continuous. Payment methods proliferate, non-salary vendors get paid faster than ever, and cash balances can swing by double digits in a week. For legal practices, the complexity multiplies with trust accounting and matter-level billing that must remain pristine to satisfy bar rules and client audits. This speed and complexity make manual controls insufficient. The firms that outperform are building live, data-connected risk visibility and automating their highest-friction controls—without adding headcount.

Think of it as moving from a rearview-mirror workflow to a forward radar system. Instead of spotting issues after month-end, you detect anomalies within hours. Instead of redoing reconciliations for days, you rely on continuous bank feeds and rules-based matching. Instead of scrambling through emails and PDFs to answer an auditor, you export a tamper-evident trail in minutes. That shift is the heart of modern small-business and small-firm risk management.

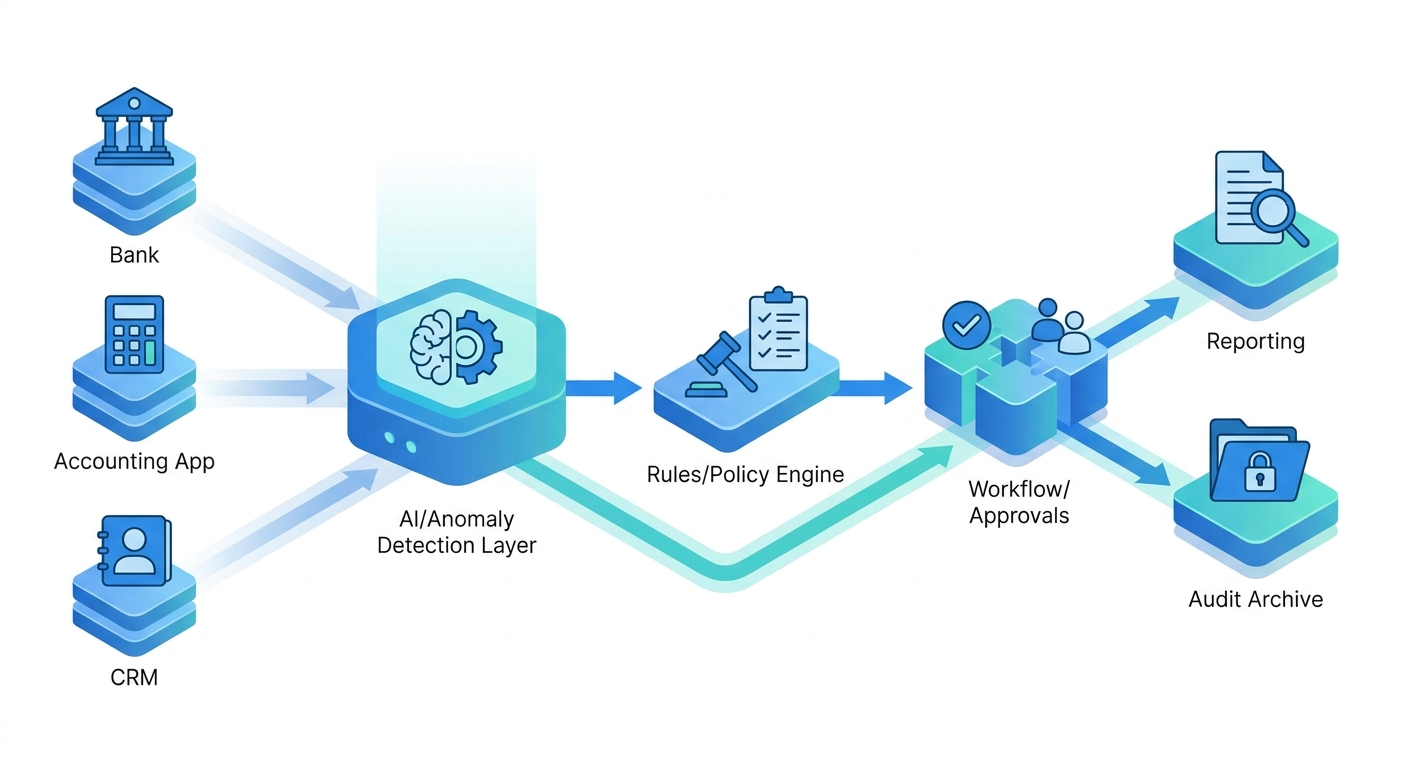

What Modern Tools Like Pillar Actually Do

New financial risk management platforms bring together the data, analytics, and workflows that used to live across spreadsheets, accounting systems, bank portals, and inboxes. While offerings differ, leaders in this category—including tools like Pillar—typically provide four core capabilities:

- Unified data layer: Secure connectors to bank accounts, accounting ledgers, billing systems, and payment processors stream live transactions and balances into a single, normalized view. This breaks the “copy/paste and reconcile” cycle.

- Automated controls: Rules-based approvals, segregation of duties, user access controls, and configurable thresholds (e.g., “flag any vendor payment >$5,000 made outside normal hours” or “alert if trust balance approaches matter-level minimum”).

- Risk analytics and alerts: Real-time anomaly detection, cash flow scenario modeling, and counterparty concentration views that highlight where a late payment or chargeback could ripple through operations.

- Audit-ready evidence: Immutable activity logs, standardized reports, and time-stamped decisions that collapse audit prep from weeks to hours and reduce compliance anxiety.

For legal practices, specialized features frequently include trust/IOLTA guardrails (three-way reconciliation support, matter-level sub-ledgers, and disbursement safeguards) and configurable workflows that separate attorneys’ billing authority from disbursement approval. For other professional services and owner-led companies, the same foundations strengthen vendor management, expense controls, and revenue collection predictability.

Use Cases: Fast Wins for Small Businesses and Legal Practices

1) Stabilize cash with forward-looking visibility

Most firms forecast by extrapolating last month. A better approach is to merge expected receivables, committed payables, and seasonality into a rolling 13-week forecast. Modern tools consume invoice statuses, bank debits/credits, and payroll schedules automatically; scenario switches (e.g., “what if Client A pays 15 days late?”) expose cash cliffs before they appear. Result: fewer emergency draws and better terms with lenders.

2) Close the loop on payment risk

Chargebacks, duplicate payments, and vendor changes are expensive—and often invisible until after settlement. Risk platforms can enforce vendor-change controls (two-person verification), flag out-of-pattern refunds, and watch for duplicate invoice numbers or bank details. Alerts route into a lightweight workflow so the right person can respond fast.

3) De-risk trust accounting and client money

For law firms, a single misapplied trust disbursement can jeopardize licensure and reputation. Systems that align matter sub-ledgers with bank balances and operating books—plus require documented approvals—reduce the chance of error and make it simple to furnish proof to clients or auditors. Role-based access limits who can initiate, approve, and reconcile.

4) Strengthen vendor and counterparty oversight

Concentration risk creeps up quietly. A dashboard that shows the percent of revenue tied to a handful of clients—or the portion of spend running through one critical vendor—helps owners diversify deliberately. With automated alerts, a deteriorating payment pattern on a top customer triggers conversations before it becomes a collections issue.

Your RiskOps Blueprint: A Lightweight, Durable Stack

“RiskOps” adapts DevOps-style principles—automation, observability, and continuous feedback—to the financial backbone of a small firm. You don’t need an army of analysts to benefit. Start lean, automate the riskiest manual steps, and institutionalize what used to live in a senior partner’s head.

A pragmatic checklist to design your stack

- Map critical money flows: Receivables, payables, payroll, taxes, retainer/advance funds, trust accounts, and credit lines. Note owners, systems, and bottlenecks.

- Define top 10 failure modes: Examples: client pays 30 days late; duplicate vendor payment; ACH fraud; trust-to-operating mispost; missing W-9/1099 data.

- Choose your system of record: Keep accounting as the ledger of truth; your risk platform should read from and write back reconciled states where appropriate.

- Automate first-line controls: Bank-feed ingestion, vendor master changes, amount/date thresholds, and two-person approval for sensitive actions.

- Establish real-time observability: Dashboards for cash runway, receivables aging, trust balances by matter, vendor concentration; subscribe key leaders to daily/weekly digests.

- Codify exceptions workflow: Who gets alerted, how they triage, what evidence is captured, and how resolutions close the loop in accounting.

- Design for audits from day one: Immutable logs, exportable reports, and clear role definitions. Every control should produce evidence automatically.

- Test with tabletop exercises: Simulate a late-payment shock, a suspicious vendor change, and a trust disbursement edge case; refine thresholds and roles.

Key capabilities to prioritize in a platform like Pillar

- Bank-grade connectivity and permissions: Read/write scopes, MFA support, and granular roles for initiators, approvers, and auditors.

- Scenario modeling: Toggling assumptions for receipts, payment dates, and contingency outflows to reveal best/likely/worst cash paths.

- Policy-as-rules: Translate firm policies (e.g., “No trust disbursement without signed authorization”) into system-enforced gates.

- Workflow and evidence capture: Approvals, comments, attachments, and time stamps tied to each transaction and exception.

- Open architecture: Connectors to accounting, billing, document management, and identity providers to avoid swivel-chair processes.

Implementation Roadmap and ROI Modeling

You can make tangible progress in 90 days without pausing operations. Here’s an execution plan that balances speed with control rigor.

Days 1–30: Baseline and quick wins

- Connect read-only bank feeds and accounting to centralize visibility; validate data freshness and identity permissions.

- Stand up a 13-week cash forecast; compare model versus actuals weekly to tune assumptions.

- Enable high-signal alerts only (e.g., duplicate invoice numbers, large after-hours payments, trust balance variance).

- Document a two-step approval for vendor master changes and trust disbursements.

Days 31–60: Automate controls

- Roll out rules-based approvals by amount, vendor, and account type; capture supporting documents in-line.

- Integrate billing and timekeeping (for firms) or e-commerce/CRM (for businesses) to tighten the receivables pipeline.

- Pilot scenario analysis for top five clients and top ten vendors; build playbooks for late-payment and supply delay events.

Days 61–90: Harden and audit

- Refine roles/permissions, enforce MFA, and finalize exception workflows with SLAs.

- Run a mock audit: export evidence logs, reconcile trust accounts, and verify completeness with management sign-off.

- Publish a one-page RiskOps policy to train staff and new hires.

How to compute ROI (an illustrative approach)

Many firms justify the investment by quantifying avoided losses and time saved. Use conservative assumptions and revisit every quarter.

| Benefit Category | How to Measure | Example Inputs (Illustrative) | Annualized Impact |

|---|---|---|---|

| Reduced leakage (duplicate/erroneous payments) | Before/after exceptions per 1,000 invoices | From 4 to 1; avg. error $1,200 | 3 fewer x $1,200 x 12 months = $43,200 |

| Faster collections | Days Sales Outstanding (DSO) reduction | DSO from 45 to 40; $3M revenue | ~$410/day interest-equivalent on freed cash |

| Staff time saved on reconciliations | Hours per month spent reconciling | 40 hours → 16 hours; $45/hour burdened | 24 x $45 x 12 = $12,960 |

| Audit readiness | Preparation days avoided | 5 days saved; $800/day blended | $4,000 |

Sum your firm’s actuals, subtract software and change-management costs, and express ROI as (Net Benefit ÷ Total Cost). If the payback exceeds one year, look for scope reduction or staged rollout to capture quick wins first.

Comparison: Ways to Manage Financial Risk

| Approach | Time to Implement | Visibility | Controls & Approvals | Audit Trail | Ongoing Effort | Best Fit |

|---|---|---|---|---|---|---|

| Spreadsheets + Email | Immediate | Low; siloed | Manual; error-prone | Fragmented | High | Very small teams, temporary stopgaps |

| ERP Add-Ons | 2–6 months | Medium; ERP-bound | Moderate; often IT-led | Good if used consistently | Medium | Mid-size firms standardized on one suite |

| RiskOps Platforms (e.g., Pillar) | 2–8 weeks | High; cross-system | Strong; policy-as-rules | Excellent; immutable logs | Low–Medium | Small businesses and legal practices needing speed + rigor |

Governance, Compliance, and Vendor Selection Pitfalls

Automation is powerful—when grounded in sound governance. Before you switch on auto-approvals, define who can create vendors, who can approve disbursements, and who can reconcile. Enforce multi-factor authentication and least-privilege access across every integrated system. For legal practices, map your rules to trust accounting standards and ensure your workflows produce matter-level documentation by default.

Cash flow is the most sensitive risk signal in a small organization. The goal isn’t eliminating volatility—it’s detecting, deciding, and documenting faster than risk can compound.

Vendor evaluation checklist

- Security and compliance: SOC 2 or equivalent reports; encryption in transit/at rest; role-based access; SSO/MFA; data residency options.

- Connectivity: Native connectors for your bank(s), accounting, billing, and document systems; webhooks; API rate limits and reliability SLAs.

- Workflow depth: Can policies become rules without custom code? Can you bundle evidence and comments with each decision?

- Audit support: Immutable logs, versioned policies, and export formats accepted by auditors and bar associations.

- Legal-specific features (if applicable): Matter sub-ledgers, trust/IOLTA safeguards, three-way reconciliation assistance, and configurable approvals for disbursements.

- Total cost of ownership: Clear pricing, admin overhead, and change-management support (templates, training, and playbooks).

- Roadmap and vendor stability: Transparent release cadence, uptime history, and a clear plan for AI explainability and bias controls.

Common pitfalls to avoid

- Turning on every alert: Start with 3–5 critical rules; grow carefully to prevent alert fatigue.

- Automating bad processes: Fix policy gaps first; codify, then automate.

- Ignoring people and training: Document how exceptions are handled; rehearse with tabletop drills.

- Underestimating data quality: Establish naming conventions, vendor master stewardship, and month-end reconciliation hygiene.

Conclusion: Put RiskOps to Work—Without Slowing the Work

Financial risk will never be static, but your operating discipline can be. By implementing a modern risk management platform—such as Pillar—and adopting a RiskOps mindset, small businesses and legal practices move from reactive cleanup to proactive control. Start with live visibility, automate a handful of high-signal controls, and build audit-ready evidence as a natural byproduct of daily work. Within 90 days, you can stabilize cash, reduce leakage, and make better decisions with less anxiety. The ultimate win isn’t just lower risk; it’s the confidence to pursue growth, hire earlier, and negotiate from strength.

Ready to explore how you can streamline your processes? Reach out to A.I. Solutions today for expert guidance and tailored strategies.